Words matter. But in economic discussion as elsewhere they are frequently abused. In economic commentary one of the most frequent falsehoods is to describe speculative activity as investment. Stock market ‘investors’ are in fact engaged in speculative activity. There is no value created by this speculation. The claim made by its apologists that it provides for the efficient allocation of capital to productive enterprises is laughably untrue in light of both recent events and long-run history. In fact, a vast number of studies show that that there is an inverse correlation between the growth rate of an economy and the returns to shareholders in stock market-listed companies.

Words matter. But in economic discussion as elsewhere they are frequently abused. In economic commentary one of the most frequent falsehoods is to describe speculative activity as investment. Stock market ‘investors’ are in fact engaged in speculative activity. There is no value created by this speculation. The claim made by its apologists that it provides for the efficient allocation of capital to productive enterprises is laughably untrue in light of both recent events and long-run history. In fact, a vast number of studies show that that there is an inverse correlation between the growth rate of an economy and the returns to shareholders in stock market-listed companies.

The chart below is just one example of these studies, Fig. 1. The research from the London Business School and Credit Suisse shows the long-run relationship between real stock market returns and per capital GDP growth. The better the stock market performance, the worse the growth in real GDP per capita. The two variables are inversely correlated.

The Economist found this result ‘puzzling’. But it corresponds to economic theory. The greater the proportion of capital that is diverted towards speculation and away from productive investment, the slower the growth rate will be, and the slower the growth in prosperity (per capita GDP).

This is exactly what has been happening in all the Western economies over a prolonged period. SEB has previously identified a declining proportion of Western firms’ profits devoted to investment. The uninvested portion of this capital does not disappear. Instead, it is held as cash in banks and the banks themselves use this to fund speculation and share buybacks by companies (which simply omits the banks as intermediaries in the speculation). The effects of this are so marked that some analysts believe ‘financialisation’is the cause of the current crisis, when instead it is an extreme symptom of the decline in investment and the consequent growth of speculative activity.

Stock market crashes

It is now customary in the Western financial press to routinely ascribe all aspects of the Great Stagnation to some failing in China. So, China’s fractional currency devaluation has been identified as the culprit of the recent stock market plunges, even though the 3% devaluation of the Chinese RMB followed a 55% of the Japanese yen and a 27% decline in the Euro.

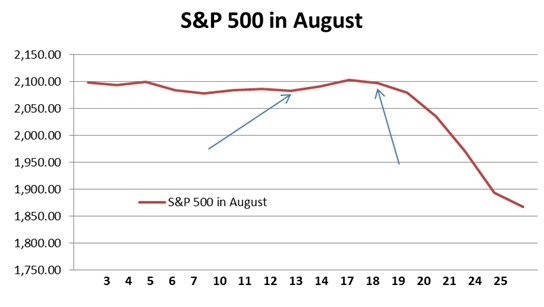

The claim that the crashes were caused by China’s currency move has no factual basis. Fig.2 below shows the closing level of the main US stock market index in August. The S&P 500 rose from 2,083 to 2,102 in the 4 days after the RMB’s 3.2% devaluation which finished on August 13 (first arrow).

On August 19 the Federal Open Markets Committee (FOMC) of the US central bank released the minutes of its most recent meeting (second arrow), which was widely interpreted as indicating a strong likelihood that interest rates would be increased in September. The prior closing level for the S&P500 was 2,097 and it fell sharply thereafter. Following speeches by a number of governors of the US Federal reserve (who vote on the FOMC) questioned the need for an increase in rates, and the market has recovered in response. Yet other speeches pointing once more to a rate rise led to stock market falls once more, and so on.

There is a spearate matter that the US economy does not look robust enough to absorb any significantly higher interest rates, but this hardly concerns stock market speculators. Fig. 3 below shows the pace of growth in US industrial production versus the same month a year ago. Production has slowed for a year and is down to a snail’s pace in the last 3 months, averaging less than 1.4% from the same period a year ago. The latest data show that the US economy is experiencing only modest growth, with GDP in the 2nd quarter just 2.6% higher than a year ago.

Despite the widespread hype about the British economy, the equivalent data on industrial production is growth of 1.5% for the latest 3 months compared to a year ago. For the Eurozone it is 1.2%. In China, industrial production has grown by 6.3% in the latest 3 months compared to the same period a year ago.

Corbynomics and crashes

Since 2010 the major central banks of the US, Japan, and the Eurozone have created US$4.5 trillion, Yen 200 trillion and €1.1 trillion in their respective Quantitative Easing programmes. The Bank of England has added £375bn of its own. Over the same period short-term official interest rates have been at or close to zero. Long-term interest rates have also plummeted. This has not led to a revival of investment in the advanced industrialised economies. After the short-lived stimulus in some Western economies to end the 2008-2009 slump, total fixed investment (Gross Fixed Capital Formation) has slowed to a crawl in the OECD as a whole, as shown in Fig.4 below.

Yet over the same period the main stock market indices in the OECD economies have soared. The stock markets and real GDP are inversely correlated. The S&P500 index has effectively doubled since 2011. The Eurofirst 300 has risen by 55%, the Nikkei 225 in Japan has risen by 125% (boosted by currency devaluation) and the FTSE100 has risen by 25% (a poorer performance held back by the predominance of weak international oil and mining stocks). Data for 2014 is not yet available but the total cumulative increased on OECD GFCF from 2011 may not have reached 10%.

Corbynomics is the policy of attempting to address an investment crisis with an increase in investment. Its critics repeatedly claim that this policy will cause financial turmoil. In light of recent events this assertion ought to cause a wry smile. At the very least, the most powerful central banks in the world have to reassess their intentions on policy simply because of the wild gyrations in the stock markets. These have been accompanied by further large movements in global currency exchange rates.

The reason stock markets are so febrile, and policy so easily blown off course is that a bubble is being created in financial assets because of the combination of monetary creation, ultra-low interest rates and weak investment. Capital that could be directed towards increasing the productive capacity of the economy is instead being used to finance speculation; the worst of both worlds. This policy has caused inflation in financial assets such stock markets, in house prices and (previously) in commodities prices. But continued economic stagnation means that deflation is now the greater risk in the OECD economies at the level of consumer prices.

Corbynomics addresses those risks because its aim is to raise the level of investment in the economy. By increasing the productive capacity of the economy through investment-led growth it overcomes the weakness of the economy. By redirecting the flow of capital from speculation towards investment, it deflates the speculative bubble. So, to take an obvious example, by building new homes it provides housing and employment while deflating the house price bubble.

The root of the objection to Corbynomics is the insistence that the private sector, private capital must be allowed to dominate the economy in its own interests. But the current Western economic model is a combination of shopping and speculation, leading to stagnation. Corbynomics is the antidote to these; prosperity through investment-led growth.

This article first appeared at Socialist Economic Bulletin

{kind=link}

{kind=link}

I have a mass of questions about this article. Here’s a few of them.

(1) In the first paragraph we are warned not to confuse investment with speculation. Are these mutually exclusive categories? Cannot there be speculative investment?

(2) We are told that speculation creates no value. This implies, in the context, that investment, by contrast, does create new value. Is that what is meant? If so does it not hark back to the old ‘factors of production’ theory of value creation?

(3) It is difficult to understand economic trends given all the competing analyses and different statistics. Therefore the highest level of clear expression is required. “Production has slowed for a year and is down to a snail’s pace in the last 3 months, averaging less than 1.4% from the same period a year ago.” does not mean what it says since that would make no sense. It means “The rate of growth of production has slowed down i.e. output is still going up but not as fast as previously.”

(4) What does “In China, industrial production has grown by 6.3% in the latest 3 months compared to the same period a year ago.” mean? Did it grow 6.3% in three months? Does it mean that in a three month period p.a. increases were consistently 6.3%? If it the later why not say so?

(5) Does “total fixed investment (Gross Fixed Capital Formation) has slowed to a crawl” mean that the value of capital invested has remained roughly constant (only a small increase).

(6) The claim that “The stock markets and real GDP are inversely correlated.” contradicts the earlier, and more plausible, that stock market changes are inversely correlated.

I could go on but that’s enough.

In the middle of all that I suddenly find myself on solid ground as as it were:

(2) We are told that speculation creates no value. This implies, in the context, that investment, by contrast, does create new value. Is that what is meant? If so does it not hark back to

I appreciate that things are no longer that simple, (particularly in this new era of fiat currency and leveraged assets and, “all that stuff,”) but I still think that those, “old, (which is to say familiar and perhaps reassuring; to someone of my pre crash my generation,) ‘factors of production’ theory of value creation,” may still have the last laugh as it were.

As things stand, (and this is always the endgame of Globalization; which is to say of American foreign and economic policy everywhere,) the UK currently produces almost nothing of value and we own no real assets or resources and we seem to be hurtling towards Thatcher’s neolibral nightmare of a typical low wage service economy, exactly like Mexico, or any of the South American or Third World hell holes that the US have created.

My last sentence above seems to have become mangled. It should have read

The claim that “The stock markets and real GDP are inversely correlated.” contradicts the earlier, and more plausible claim, that stock market returns are inversely correlated with the growth of GDP.

I always like Michael’s posts.

I have already voted for Jeremy and watching the Sky debate tonight thought Cooper was sounding desperate.

I thought Jeremy did excellent and so did 80% of a relatively small sample of 8,000 viewers who contributed on-line.

I hope Jeremy wins and hopefully quantitative easing for investment will work.

But policy tools we could also consider are getting our expropriated share of the wealth back from big business via Windfall Taxes, EC/Global Common Corporate Taxes, fair taxes on the rich & land and a significant EC Financial Transaction Tax.

Plus democratic socialist parties in every country in the World fighting for similar things such as a global living wage and a shorter working week plus democratic public ownership by country with staff and communities having a say- MORE DEMOCRACY WILL BEAT NEO-LIBERALISM!

Yours in solidarity!

Why do you think Cooper sounded desperate?

This is sailing dangerously close to the `no more boom and bust’ bollox of Gordon Brown. In fact more investment in a market collapsing from overproduction will just give rise to more overproduction and a swifter crash. There can be no technical fix to the class struggle. Print money and you devalue it simple as. Ask the Weimar Republic. Of course austerity is destroying the real economy very quickly and in fact represents the greatest redistribution of wealth from poort to rich in history at a time when exactly the opposite is required but stimulation will have exactly the same result in the end as the 2008 collapse showed. There is only one cure for capitalism and that is communism. The dispropriation of the rich and the socialisation of the means of production and exchange.

Clever economic nonsense cannot substitute for class struggle. Let’s not replace cynical realism with cynical idealism.

The appropriate economic response to the collapse and liquidation of the means of production is neither austerity or stimulus both of which end in the same place i.e. the immiseration of the masses, but consolidation. That means taking the means of production into the protective custody of the working class and redistributing the wealth from rich to poor. Save the real economy from the Bankers’ Versailles.

Yes it’s so simple, ma chouette

Perhaps; although all people I’ve spoken to who’ve actually lived under communism in Eastern Europe, (whilst some of them still acknowledging that it’s great and worthy aspiration of the human spirit in some happy, “ideal,” world,) they were all and entirely without exception happy to finally see the back of it.

Nonetheless, I largely agree with your argument that the state should stand a custodian, a guarantor and a policeman of the interests of all the people living in the UK, particularly, not just the richest few and particularly so of the welfare, rights and interests of poorest who are by contrast the majority; underrepresented, increasingly exploited and often simply just excluded.

I believe very much in the socialist principle, (hard won and abandoned far too easily by Labor,) of social security and a safety net and of state ownership and control of key sectors in the public interests, which would include Defense, Policing, the NHS, not for profit Social Housing and so on.

Once the poorest and so particularly the disabled and those most financially and socially vulnerable have been as adequately protected as is practical and sensible for us to do as a society, then yes by all means I have no objection to people who want to, “getting filthy rich,” provided they’re not simply just successful criminals.

In this context for example, the continued liberty of both Tony Blair and of Steven Green continues to be deeply problematic to many people, considering their well known track records of, well evil, (although not always criminal,) might not be too strong a term for it, (particularly as financial crime on that scale is never as victim-less as some people might like to pretend.)

But QE is not printing money its electric, so far we have had £3Billion plus, all going to the banks, the currency has stayed pretty stable, why should the same not happen when it targets government developement projects? Or is the city going to sabotage it as it prefers another crash rather than a sucsessful socialist government.

People are commenting on this post (article) as if its content is completely clear to them. To me it is far from that and I listed points on which I would like clarification. I may be exceptionally thick but I try to understand these things and would appreciate some help from those who apparently understand everything that Michael Burke says in this piece.

I have put direct questions. It would have been in the best traditions of democratic debate if the author had deigned to respond. But that is a rare event, even on left-wing websites like this one – more’s the pity. So how about someone else helping me out?

Overall, I take this sort of thing as a worrying sign that the most people on the left just doesn’t see the difference between real open and informed democratic debate and having the things (nostrums?) they favour brought to the foreground.

Questions about economic policy, on this website, which at least has the honour of highlighting many issues not highlighted elsewhere, nearly always go unanswered. What does that tell us about the likely quality of debate of economic debate if Corbyn is elected (which I very much hope that he will be)?

We have a long way to go to be up to the task of supporting and sustaining a Corbyn leadership.

I share your pain.

However it is probably worth noting that level of, (almost academic,) debate occurring here on economic policy is sometimes pretty opaque to most, “lay people,” to start with, for as I commented above whilst I’m on fairly firm intellectual ground with, “the old ‘factors of production’ theory of value creation,” and I’ve even made the occasional tentative foray into Marx and Adam Smith much of it seems like the kind trendy overblown theory that comes and goes almost with the weather.

I think that as well as polemic and analysis, there is also a need here to educate and inform, (to explain clearly,) about these topics as well, particularity if the left are serious about connecting and engaging with people outside the charmed circle of the chosen few who too often seem to be full time, (I hesitate to use the term Ivory Tower,) academics or similar.

Certainly the views and experiences of disabled people or people scraping a precarious living on a zero hour contract, (which is to say no contract at all,) or doing part time work, being bullied, cheated and and otherwise abused by the DWP etc and saddled with debt, to be of little or no interest and of no relevance to many of the people posting comments here.

“Hearing the news ain’t like being there,

Nothing is real unless it’s happening to you?”